First and foremost, we are sorry for your loss. Surviving spouse options – when someone leaves behind a spouse and retirement accounts we need to of course grieve. We also falsely assume that the financial advisor knows best what surviving spouse options exist. This assumption can and will get you in trouble. There are many factors to consider in what to do with inherited retirement accounts.

Please know that you don’t have to move the account(s) until, at the earliest, September of the year following the year of death. We use our 15 page checklist to ensure we all understand all of the variables and can make the best choice possible.

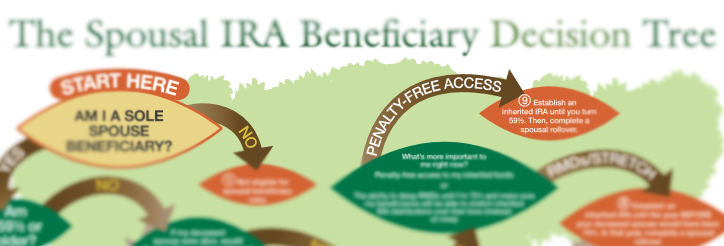

NOTE: The IRS does grant surviving spouses some leeway in fixing mistakes. Fixing mistakes is not without fees for advisors and sometimes the IRS.

In one’s time of grieving there are two details to know. 1) It may be in your best interest to leave the account in your late spouses name to avoid tax penalties (this depends ages of all parties) 2) you don’t need to move the account or retitle it until at the earliest, September (if a trust is used) in the year following the year of death – and maybe never for a spouse. NOTE: If the spouse is the sole beneficiary the account can remain untouched, but required distributions must start. If there are non-spouse beneficiaries named – we have to complete this work by December 31 of the year following the year of death.

If you would like some support regarding your situation you may complete the form below or call our office. The first call is always complementary. You can book your phone call online too.

Resources

Survivors Checklist – free download, no strings attached